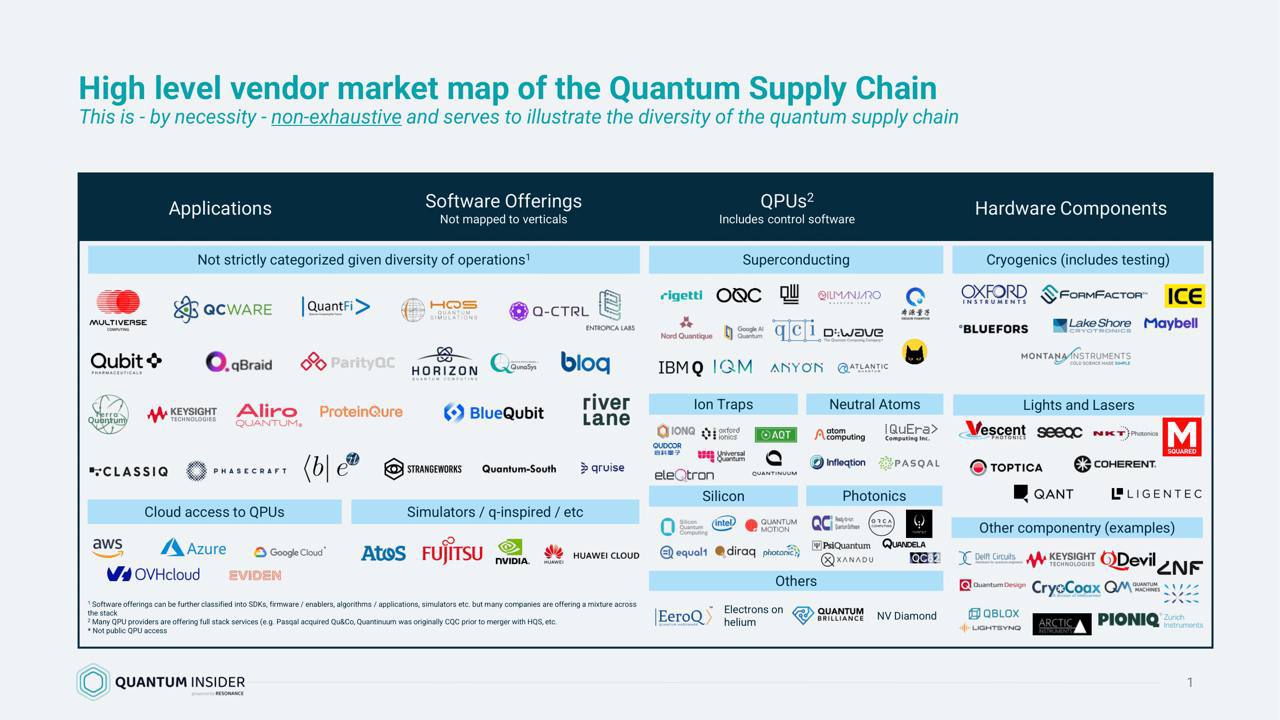

A Pragmatic Look at the Quantum Computing Supply Chain

I came across an insightful market map from The Quantum Insider that breaks down the current quantum computing landscape. In a field often dominated by news of qubit counts and theoretical breakthroughs, this provides a practical, engineering-focused view of the ecosystem that is actually being built.

It’s a clear signal that the industry is maturing beyond pure R&D and into a complex supply chain with distinct, specialized layers. Here’s a summary of the key players and technologies shaping the field, based on that research.

The Core: Quantum Processing Units (QPUs)

This is the hardware layer where computation happens. The market is currently a race between several competing architectures, with no clear long-term winner yet.

- Leaders: IBM, Rigetti, Quantinuum, IonQ, and QuEra are some of the most prominent names.

- Architectures: They use different approaches, from superconducting qubits and ion traps to neutral atoms and photonics. Much like we have CPUs, GPUs, and TPUs today, the future of computing will likely involve a hybrid of these specialized quantum processors.

The Software Layer: Bridging Hardware and Users

Raw quantum hardware is useless without a robust software layer to control it and make it accessible. This is where platforms and tools come in.

- Platforms & Tools: Companies like Q-CTRL, Riverlane, Classiq, and StrangeWorks are building the crucial software for quantum control, error mitigation, and algorithm development.

- Cloud Access: Major cloud providers are democratizing access to quantum hardware. AWS, Azure, and Google Cloud now offer services that let researchers and enterprises experiment with QPUs remotely.

The Unseen Foundation: Infrastructure & Components

Quantum computers can’t exist in a vacuum. They depend on a highly specialized supply chain of traditional hardware engineered for extreme conditions.

- Key Components: This includes cryogenics from firms like Bluefors and Oxford Instruments, along with precision lasers, and custom control electronics from companies such as Qblox and Vescent.

- Importance: Advances in these enabling technologies are just as critical as advances in qubits themselves for improving stability, coherence, and error rates.

The Goal: Real-World Applications

Ultimately, the goal is to solve real-world problems. While still in early stages, we are seeing the first wave of application-specific quantum companies.

- Finance: Multiverse Computing and QC Ware are targeting risk modeling and portfolio optimization.

- Pharmaceuticals: Qubit Pharmaceuticals and ProteinQure are focused on drug discovery and molecular simulation.

- Logistics & Cryptography: Aliro Quantum and ParityQC are building solutions for optimization and security.

The key insight here is that quantum computing is no longer a monolithic pursuit. It’s an ecosystem. The companies that succeed won’t just build a powerful QPU, but will integrate effectively into this emerging, multi-layered supply chain.

Source: The Quantum Insider - The Quantum Supply Chain: Mapping the Market and Key Players